Two years since the pandemic shock helped drive global share markets down 30-40% in the space of weeks, volatility is back.

This time, however, it’s war, inflation, and recession fears that are dominating headlines, and not even bonds are immune. It’s a worrying time for investors, to be sure. But just as in every crisis, discipline is the key.

It can be psychologically tough not to panic and succumb to a knee-jerk response when markets are experiencing a substantial drawdown like we have seen this year. Stress levels are naturally high and the temptation to “do something” can feel over-powering.

But history suggests that those investors who keep their nerve, stick to their agreed financial plan, and maintain focus on their chosen horizon at these times tend to do significantly better than those who sell assets that have already fallen in price.

We only have to go back to the events of 2020 to see the value of staying the course. The headlines in March of that year spoke of catastrophic outcomes. The Sydney Morning Herald, predicting the worst depression since 1932, quoted economists as saying unemployment was headed to 15% or more.*1

The pandemic combined with an oil price war and recession fears to drive $9 trillion from global equities in days.

Of course, we now know with the benefit of hindsight that the Australian economy actually performed relatively well through the pandemic, with unemployment, after a brief spike, heading to historic lows. Global equities bounced later in the year as vaccines emerged so that by November major benchmarks were back at record highs.*2

Of course, this time is different. The circumstances are always different.

The pandemic disrupted global supply chains just as massive fiscal and monetary stimulus was firing up demand. The war in Ukraine added another dimension, with prices of oil, food, gas and other commodities soaring. Inflation in many developed economies has reached levels not seen in decades. And central banks, after confidently predicting a year ago that inflation would be transitory, are now aggressively lifting benchmark interest rates.

While bond yields and credit spreads spiked briefly in the crisis of March 2020, they came back down after a couple of months and offered a cushion to the shock in equity markets.

This time, market interest rates have risen well in advance of central bank official rates and have kept rising even as equities have continued to fall. As a result, even those investors in relatively conservative portfolios have suffered as inflation expectations have ratcheted higher.

Compounding the hit to sentiment, investors in global equity markets have been worrying that the medicine of higher interest rates will be worse than the disease, driving developed economies into a deep recession.

So this is not 2020 all over again. We can’t be confident there will not be further volatility and the news can get worse before it gets better. But while every crisis is different, the best response for investors is always the same:

Focus on what you can control.

Here are seven lessons to keep in mind:

Lesson 1

While you may be tempted to take refuge in cash “until the storm passes”, market timing is difficult to pull off. You risk turning paper losses into real ones and missing the bounce when it comes.

For example, the second worst month for the S&P/ASX 300 index was the near 21% fall in March, 2020. But its 12th biggest rise came a month later when it rose 9%. In November that year, it rose 10%, its ninth biggest increase.

Bonds are tough to time as well. The single best month for the global bond market in the past three decades was the 3.7% surge in May, 1995, but this came after the fourth and fifth worst months a year earlier.

Lesson 2

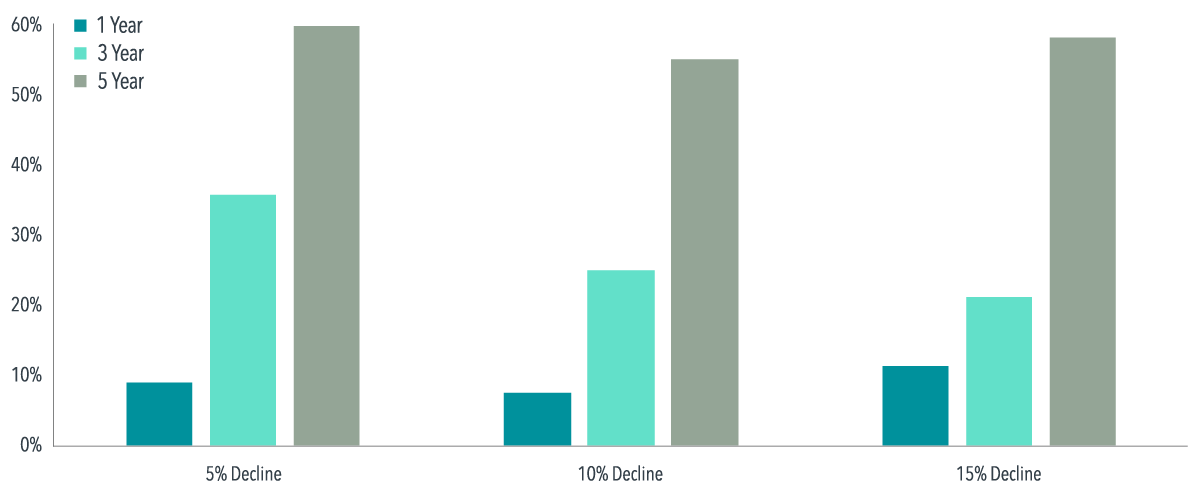

Balanced portfolios have quickly regained losses after past significant declines in the past.

The chart below shows the subsequent performance of a balanced Australian 60/40 portfolio after periods of 5%, 10% and 15% declines going back to 1985.

While care needs to be taken with these comparisons due to the small number of examples – only two over 37 years in the case of 15% – this also highlights how rarely a balanced portfolio experiences significant declines.

EXHIBIT 1

Average Returns After Downturns Have Been Positive

AUD 60/40 Balanced Portfolio, Jan 1, 1985 – May 31, 2022

Past performance is not a guarantee of future results. See sources of data and descriptions below.

Lesson 3

The recent past doesn’t tell us anything about future returns. Prices of shares and bonds have adjusted lower in recent months.

That means that all else equal, expected returns are higher than they were late last year. If the news going forward – on issues like inflation, economic growth and earnings – is better than what is currently reflected in prices, asset prices could adjust higher.

In this context, remember that what moves markets the most is news it didn’t expect.

Lesson 4

While market timing can be counter-productive, you can still use the opportunity of lower prices for stocks and bonds to rebalance your portfolio back to your chosen allocation. This, however, is part of a disciplined, regular and structured process, not a knee-jerk response to volatility.

Lesson 5

Recessions are always identified with a lag. And even if there is one, the record shows that markets are often on their way to a recovery by the time the recession is confirmed.

That’s another argument for staying disciplined.

Lesson 6

In any case, even in tough economic environments innovation and wealth creation continue. Companies still bring together raw materials, technology, labour, intellectual and financial capital to develop new products and services that create wealth for shareholders.

Governments and companies still need to raise funding in bond markets to deliver services and build long-term infrastructure. Investors who participate in bond and equity markets have an opportunity to share in the wealth created while financing those developments.

Lesson 7

Finally, a well-constructed financial plan will make allowances for periods like the present and is shaped according to the risk appetites and goals of each individual.

The right plan will help you see past the daily news headlines so you can stick it out through the tough times to get to the good times on the other side.

Uncertainty is a constant. But if there were no uncertainty, there would be no return. And while the good times don’t last forever, neither do the bad.

There is no downplaying the emotional effect of times like this when even the fixed interest part of your portfolio is showing negative returns. But these times, while unwelcome, are not unprecedented or unexpected.

As ever, diversification, discipline and sticking to your agreed plan, with regular balancing, is still the best course to navigate this or any storm.

The author thanks Investment Associate Chloe Lam, Senior Portfolio Manager Slava Platkov and Senior Researcher Warwick Schneller for their assistance with this article.

Exhibit 1 Disclosures

Returns In AUD. Balanced Strategy: 30% S&P/ASX 300 Index (total return), 30% MSCI World ex-Australia Index (AUD, net div.), 20% Bloomberg AusBond Bank Bill Index and 20% FTSE World Government Bond Index 1-3 Years (hedged to AUD) for the period January 1985 – April 1990; 30% S&P/ASX 300 Index (total return), 30% MSCI World ex Australia Index (AUD, net div.), 20% Bloomberg Global Aggregate Bond Index (hedged to AUD), 20% Bloomberg AusBond Composite 0-5 Yr Index for the period May 1990 – May 2022. Rebalanced semi-annually.

Compounded returns are calculated for the 1-, 3-, and 5-year periods beginning the first month after a downturn of 5%, 10%, or 15% from a new all-time month-end high for the portfolio. The bar chart shows the average total returns for the 1-, 3-, and 5-year periods following the 5%, 10% and 15% thresholds. For the 5% threshold, there are 9, 8, and 7 observations for the 1-, 3-, and 5-year periods, respectively. For the 10% threshold, there are 4, 3, and 3 observations for the 1-, 3-, and 5-year periods, respectively. For the 15% threshold, there are 2 observations for 1-, 3-, and 5-year periods.

Footnotes

*1 Worst Since 1932: Two Million Aussies Face Unemployment Queue’, SMH, 23 March 2020.

*2 Global Stock Markets Surge After Pfizer Covid Vaccine News’, The Guardian, 9 Nov 2020.

Disclosures

The information in this material is intended for the recipient’s background information and use only. It is provided in good faith and without any warranty or representation as to accuracy or completeness. Information and opinions presented in this material have been obtained or derived from sources believed by Dimensional to be reliable and Dimensional has reasonable grounds to believe that all factual information herein is true as at the date of this material. It does not constitute investment advice, recommendation, or an offer of any services or products for sale and is not intended to provide a sufficient basis on which to make an investment decision. Before acting on any information in this document, you should consider whether it is suitable for your particular circumstances and, if appropriate, seek professional advice. It is the responsibility of any persons wishing to make a purchase to inform themselves of and observe all applicable laws and regulations. Unauthorised reproduction or transmitting of this material is strictly prohibited. Dimensional accepts no responsibility for loss arising from the use of the information contained herein.

This material is not directed at any person in any jurisdiction where the availability of this material is prohibited or would subject Dimensional or its products or services to any registration, licensing or other such legal requirements within the jurisdiction.

“Dimensional” refers to the Dimensional separate but affiliated entities generally, rather than to one particular entity. These entities are Dimensional Fund Advisors LP, Dimensional Fund Advisors Ltd., Dimensional Ireland Limited, DFA Australia Limited, Dimensional Fund Advisors Canada ULC, Dimensional Fund Advisors Pte. Ltd, Dimensional Japan Ltd. and Dimensional Hong Kong Limited. Dimensional Hong Kong Limited is licensed by the Securities and Futures Commission to conduct Type 1 (dealing in securities) regulated activities only and does not provide asset management services.

Risks

Investments involve risks. The investment return and principal value of an investment may fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original value. Past performance is not a guarantee of future results. There is no guarantee strategies will be successful.

Australia

This material is issued by DFA Australia Limited (AFS License No. 238093, ABN 46 065 937 671). This material is provided for information only. No account has been taken of the objectives, financial situation or needs of any particular person. Accordingly, to the extent this material constitutes general financial product advice, investors should, before acting on the advice, consider the appropriateness of the advice, having regard to the investor’s objectives, financial situation and needs. Investors should also consider the Product Disclosure Statement (PDS) and the target market determination (TMD) that has been made for each financial product either issued or distributed by DFA Australia Limited prior to acquiring or continuing to hold any investment. Go to au.dimensional.com/funds to access a copy of the PDS or the relevant TMD. Any opinions expressed in this material reflect our judgement at the date of publication and are subject to change.