Key Takeaways

– Liquid-alt investments claim they deliver higher potential returns and lower correlations to stocks and bonds – but have fallen short.

– From June 2006 to June 2022, they underperformed broad indices with higher volatility than fixed income.

– Investors seeking to increase expected returns and manage risk may do so more reliably using diversified stock and bond strategies.

In the face of broad equity and fixed income market downturns, some investors may be tempted by the siren call of alternatives.

These investments may include liquid alternatives, or ‘liquid-alts’, which are a subset of fund and ETF (Exchange-traded fund) investments. They offer easier-to-access exposure to alternative strategies while enticing investors with claims about higher potential returns and lower correlations to stocks and bonds.

Our data shows that for more than a decade, liquid-alts funds in the US have underperformed broad indices tracking the equity and fixed income markets. And liquid alts may do little to diversify a portfolio composed of stocks and bonds, given that many hold a subset of these traditional asset classes.

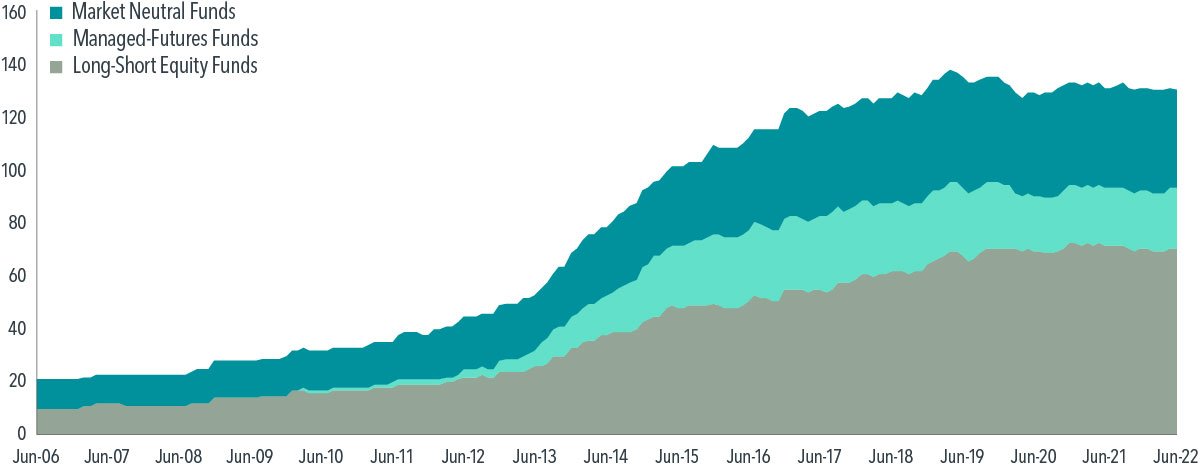

As seen in Exhibit 1, the US liquid-alts space has grown steadily over the past 16 years, from roughly 20 funds in 2006 to more than 100 in 2022.

EXHIBIT 1

Alternative Reality

Number of liquid-alternative mutual funds in the US, June 2006 – June 2022

Sample includes long-short equity, managed-futures, and market neutral equity funds from the Morningstar fund database after they have reached $50 million in AUM and have at least 36 months of return history. Multiple share classes are aggregated to the fund level. Managed-futures funds represented by the Morningstar category “US Fund Systematic Trends.” Market neutral funds represented by the Morningstar global category “Market Neutral.” Long-short equity funds represented by the Morningstar category “US Fund Long-Short Equity.”

The increasing popularity of liquid-alts cannot be traced to strong fund performance.

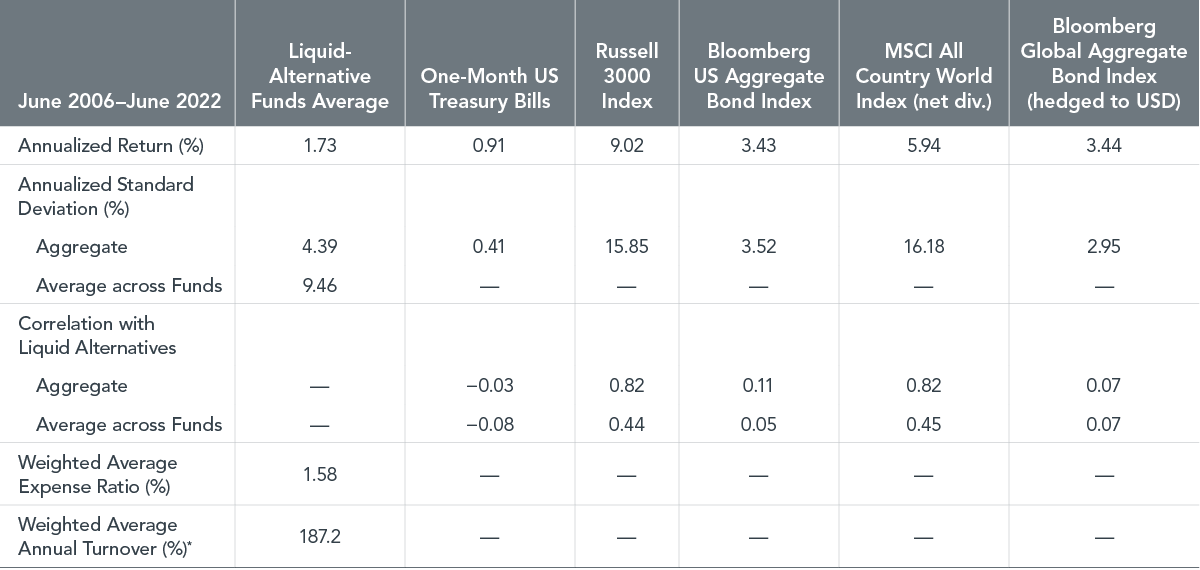

Exhibit 2 shows that the annualised return for these strategies trailed that of global stocks by 4.2 percentage points and global bonds by 1.7 percentage points from June 2006 to June 2022.

Only against one-month US Treasury Bills did liquid alts manage to eke out a slight return advantage – but with 10 times higher volatility.

Substantial costs for liquid-alts were likely a factor in their disappointing performance: The category’s weighted average expense ratio was 1.6%, with average annual turnover of 187%.(*1)

EXHIBIT 2

High and Dry

Performance and characteristics of liquid-alternative funds in the US vs. traditional stock and bond indices, June 2006 – June 2022

We believe investments belong in an investor’s asset allocation when they satisfy one of two roles: increasing expected return or managing risk.

We believe the performance of liquid-alts doesn’t check the box for the former and that their ability to fulfil the latter is questionable. Fixed income investments are better suited for reducing return volatility than liquid alts, given the latter have had close to 50% more volatility than global bonds.

It’s also not clear liquid-alts offer a diversification benefit.

Diversification arises from broadening an investor’s opportunity set. Many liquid-alternative strategies start from the same building blocks as global stock and bond markets. They then deviate in their security selection and weighting, even shorting securities(*2) in their attempt to deliver positive returns that are uncorrelated to returns in stock and bond markets.

But slicing and dicing the same set of securities doesn’t constitute expansion of the opportunity set… much like cutting my children’s pancakes in the shape of a dinosaur isn’t a culinary advancement.

What’s the Alternative?

Stock and bond markets are broadly diversified, offering investors exposure to tens of thousands of securities across more than 40 countries and different currencies.

Unlike liquid-alt claims that fall short, stock and bond markets have a track record of increasing expected returns or managing risks.

Liquid-alternatives may look attractive when traditional asset classes are down, but over time an allocation to liquid alts may leave investors high and dry.

FOOTNOTES

-

(*1)Source: Morningstar Fund data

-

(*2)A short position is the sale of a borrowed security. Short positions benefit if the borrowed security falls in value.

GLOSSARY

Market neutral: Market neutral portfolios seek income while maintaining low correlations to fluctuating market conditions. Market neutral portfolios typically hold 50% of net assets in long positions and 50% of net assets in short positions, seeking to deliver positive returns regardless of the market’s direction.

Long-short equity: Long-short equity portfolios hold both long and short positions in equities, exchange traded funds, and related derivatives, based on a macro outlook or bottom-up research. At least 75% of assets are in equity securities or derivatives.

Managed futures: Primarily trend-following, these price momentum strategies trade long and short futures, options, swaps, and foreign exchange contracts. These portfolios typically obtain exposure to a mix of global markets, including commodities, currencies, government bonds, interest rates, and equity indexes.

DISCLOSURES

The information in this material is intended for the recipient’s background information and use only. It is provided in good faith and without any warranty or representation as to accuracy or completeness. Information and opinions presented in this material have been obtained or derived from sources believed by Dimensional to be reliable, and Dimensional has reasonable grounds to believe that all factual information herein is true as at the date of this material. It does not constitute investment advice, a recommendation, or an offer of any services or products for sale and is not intended to provide a sufficient basis on which to make an investment decision. Before acting on any information in this document, you should consider whether it is appropriate for your particular circumstances and, if appropriate, seek professional advice. It is the responsibility of any persons wishing to make a purchase to inform themselves of and observe all applicable laws and regulations. Unauthorized reproduction or transmission of this material is strictly prohibited. Dimensional accepts no responsibility for loss arising from the use of the information contained herein.

This material is not directed at any person in any jurisdiction where the availability of this material is prohibited or would subject Dimensional or its products or services to any registration, licensing, or other such legal requirements within the jurisdiction.

“Dimensional” refers to the Dimensional separate but affiliated entities generally, rather than to one particular entity. These entities are Dimensional Fund Advisors LP, Dimensional Fund Advisors Ltd., Dimensional Ireland Limited, DFA Australia Limited, Dimensional Fund Advisors Canada ULC, Dimensional Fund Advisors Pte. Ltd., Dimensional Japan Ltd. and Dimensional Hong Kong Limited. Dimensional Hong Kong Limited is licensed by the Securities and Futures Commission to conduct Type 1 (dealing in securities) regulated activities only and does not provide asset management services.

RISKS

Investments involve risks. The investment return and principal value of an investment may fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original value. Past performance is not a guarantee of future results. There is no guarantee strategies will be successful.

AUSTRALIA

This material is issued by DFA Australia Limited (AFS Licence No. 238093, ABN 46 065 937 671). This material is provided for information only. No account has been taken of the objectives, financial situation or needs of any particular person. Accordingly, to the extent this material constitutes general financial product advice, investors should, before acting on the advice, consider the appropriateness of the advice, having regard to the investor’s objectives, financial situation and needs. Investors should also consider the target market determination that has been made for each financial product either issued or distributed by DFA Australia Limited prior to proceeding with any investment. Go to au.dimensional.com/funds to access a copy of the relevant target market determination. Any opinions expressed in this material reflect our judgement at the date of publication and are subject to change.