At some point over the past year, the financial media’s inflation coverage transitioned from, “Will this high inflation persist?” to, “Here’s how to cope with inflation that’s here to stay!”

It seems some investors have resigned themselves to a new normal of high inflation following decades of below-average consumer price changes.

However, financial market data tells a different story, one of potentially softening inflation.

Breakeven inflation (BEI) rates offer a window into the market’s inflation expectations. BEI is defined as the difference between yields on nominal and inflation-protected bonds of the same maturity.

BEI represents the inflation rate at which investors would be indifferent between the two.

If actual inflation were to exceed BEI rates, investors would be better off with the inflation-protected bond; if inflation were less than BEI, the reverse would be true.

BEI is therefore commonly interpreted as the average annual inflation rate expected over a given time horizon.(*1)

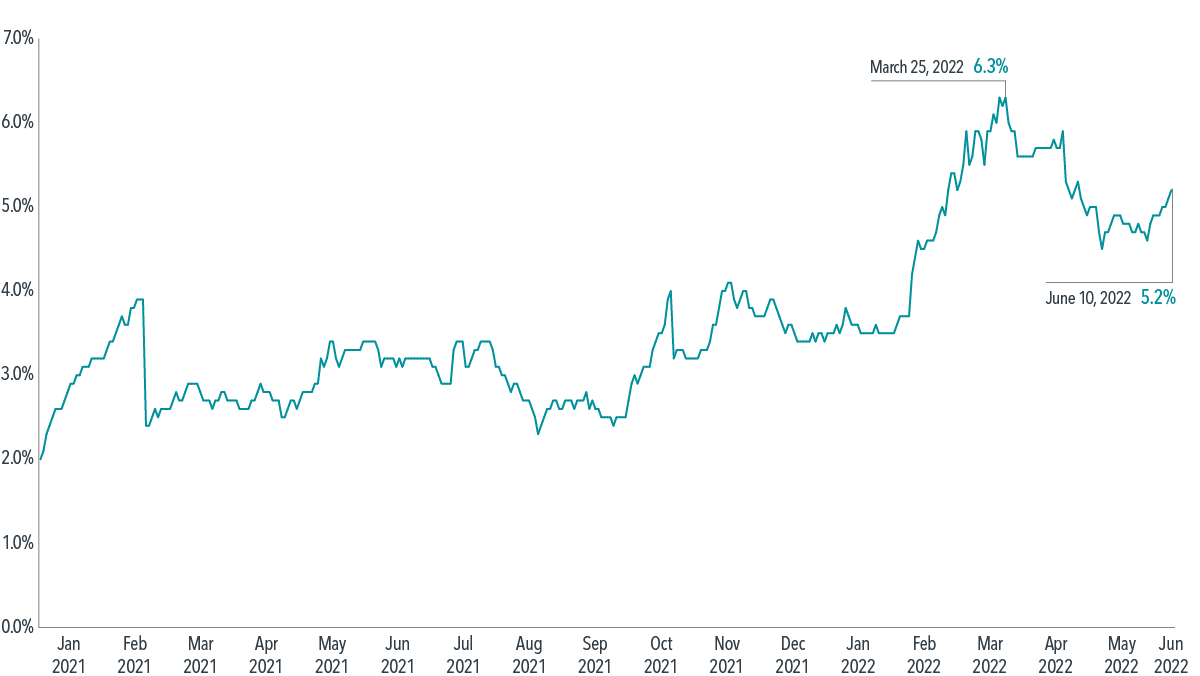

The one-year BEI shows a spike in inflation expectations this year following increasingly high consumer price index (CPI) changes. But the trajectory appears to have changed course over the past couple months (see Exhibit 1).

Since peaking at 6.3% in late March, the one-year BEI had fallen to 5.2% as of June 10.

This might be the market’s way of telling us it sees inflation getting under control in the near future.

EXHIBIT 1- Brighter Horizons

1-year breakeven inflation rate 1 Jan 2021 – 10 Jun 2022

Source: Dimensional, using data from Bloomberg

It is important to remember that realised inflation can diverge from expectations.

For example, the one-year BEI rate as of May 3, 2021, was just 2.7%. Over the next 12 months, CPI grew by 8.3%.

This means a substantial portion of this inflation seemed to have been unexpected by the market. From January 2007 to April 2022, the difference between actual inflation and that “predicted” by BEI varied from –5.59 to 8.43 percentage points.(*2)

While nominal (i.e., not inflation-protected) bond prices reflect expected inflation, investors who opt for Treasury Inflation-Protected Securities (TIPS) or approaches that overlay inflation swaps (“real return” bond strategies) get compensated for actual inflation.

Investors who want to reduce uncertainty in the event of higher-than-expected inflation may benefit from these inflation-hedging approaches.

GLOSSARY

Consumer price index (CPI):

A measure of inflation that looks at changes in the price level of a basket of goods and services purchased by households.

Treasury Inflation-Protected Securities (TIPS):

Bonds issued by the US Treasury Department that provide protection against inflation. The principal of a TIPS increases with inflation and decreases with deflation, as measured by the Consumer Price Index. When a TIPS matures, the investor is paid the adjusted principal or original principal, whichever is greater.

Inflation swaps:

An inflation-swap agreement is a two-sided contract in which one party receives floating payments tied to the actual inflation rate and pays fixed payments based on expected inflation and the inflation risk premium for a given notional amount and period.

Nominal return:

The rate of return on an investment without adjusting for inflation.

Real return:

The rate of return on an investment after adjusting for inflation.

FOOTNOTES

-

(*1)More accurately, the difference in yields between nominal and inflation-protected bonds represents both expected inflation and an inflation risk premium borne by holders of nominal bonds.

-

(*2)Based on monthly differences between one-year BEI and subsequent 12-month change in CPI for the period January 1, 2007, through April 30, 2022. CPI data from Bureau of Labor Statistics and is represented by the Consumer Price Index for All Urban Consumer (CPI-U), not seasonally adjusted.

DISCLOSURES

The information in this material is intended for the recipient’s background information and use only. It is provided in good faith and without any warranty or representation as to accuracy or completeness. Information and opinions presented in this material have been obtained or derived from sources believed by Dimensional to be reliable and Dimensional has reasonable grounds to believe that all factual information herein is true as at the date of this material. It does not constitute investment advice, recommendation, or an offer of any services or products for sale and is not intended to provide a sufficient basis on which to make an investment decision. Before acting on any information in this document, you should consider whether it is suitable for your particular circumstances and, if appropriate, seek professional advice. It is the responsibility of any persons wishing to make a purchase to inform themselves of and observe all applicable laws and regulations. Unauthorized reproduction or transmitting of this material is strictly prohibited. Dimensional accepts no responsibility for loss arising from the use of the information contained herein.

This material is not directed at any person in any jurisdiction where the availability of this material is prohibited or would subject Dimensional or its products or services to any registration, licensing or other such legal requirements within the jurisdiction.

“Dimensional” refers to the Dimensional separate but affiliated entities generally, rather than to one particular entity. These entities are Dimensional Fund Advisors LP, Dimensional Fund Advisors Ltd., Dimensional Ireland Limited, DFA Australia Limited, Dimensional Fund Advisors Canada ULC, Dimensional Fund Advisors Pte. Ltd, Dimensional Japan Ltd. and Dimensional Hong Kong Limited. Dimensional Hong Kong Limited is licensed by the Securities and Futures Commission to conduct Type 1 (dealing in securities) regulated activities only and does not provide asset management services.

Risks

Investments involve risks. The investment return and principal value of an investment may fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original value. Past performance is not a guarantee of future results. There is no guarantee strategies will be successful.

AUSTRALIA and NEW ZEALAND

This material is issued by DFA Australia Limited (AFS License No. 238093, ABN 46 065 937 671). This material is provided for information only. No account has been taken of the objectives, financial situation or needs of any particular person. Accordingly, to the extent this material constitutes general financial product advice, investors should, before acting on the advice, consider the appropriateness of the advice, having regard to the investor’s objectives, financial situation and needs. Investors should also consider the Product Disclosure Statement (PDS) and the target market determination (TMD) that has been made for each financial product either issued or distributed by DFA Australia Limited prior to acquiring or continuing to hold any investment. Go to au.dimensional.com/funds to access a copy of the PDS or the relevant TMD. Any opinions expressed in this material reflect our judgement at the date of publication and are subject to change.